The Disappearing Tail of Medical Malpractice Insurance

When American Physician Partners and NES Health declared bankruptcy, their physicians lost malpractice coverage for care they had already delivered. Why? Claims-made insurance and its tail.

The deal most emergency physicians believe they are making with their employers is the following:

The physician…

cares for patients;

documents that care in a manner that can be turned into a bill for the care delivered.

The employer…

bills either an insurer or the patient for the care delivered by the physician;

collects revenue based on the bill;

pays the physician a portion of the collections;

keeps a part to cover administrative overhead;

includes malpractice insurance within the overhead portion to protect the physician from a potential malpractice suit.

Large emergency medicine practices — American Physician Partners (APP) and NES Health — have reneged on their deals with physicians within the last two years. When APP and NES ceased operations, the companies stopped paying their malpractice carriers. Because these employers used the claims-made with tail malpractice policy type, their employed physicians’ insurance coverage for care previously delivered was terminated.

These companies left their doctors in the lurch.

Perhaps surprisingly, most physicians’ malpractice coverage is structured in the same way as APP’s and NES’s. An American Physician Partners’ employment contract included these terms: “The Practice, with the cooperation of Physician, will procure professional liability insurance, including tail coverage or post-termination coverage, as applicable based on the Practice’s insurance policy, covering Services rendered by Physician pursuant to this Agreement in sufficient limits as required by applicable state law or a Facility’s medical staff bylaws.”

How did standard-seeming contract terms lead to the loss of coverage for hundreds of physicians - twice in two years? Let’s explore.

Types of malpractice insurance

Medical malpractice insurance comes in two flavors:

Claims-made; and

Occurrence.

Both types of insurance cover expenses related to a medical malpractice suit, including legal defense costs, settlements, and judgments. The fundamental difference is that claims-made insurance is optimized for the timing and coverage priorities of the employer, while occurrence-type insurance is tailored to the physician's risk profile.

What is claims-made malpractice insurance?

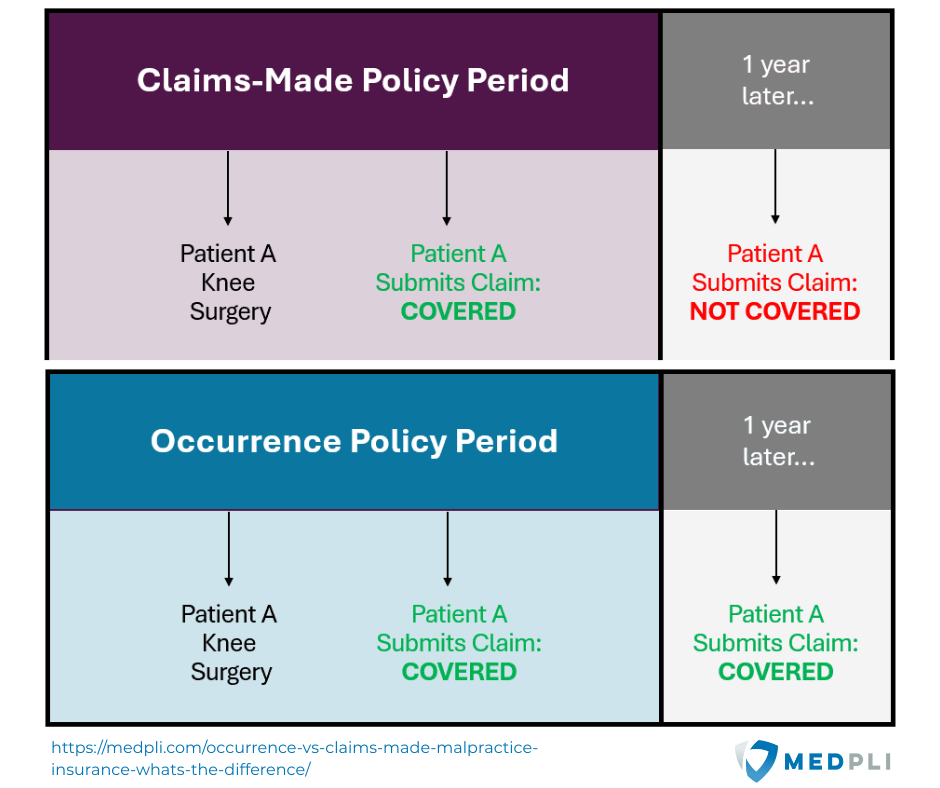

Claims-made insurance covers clinicians if the policy is in place both when an incident happens AND when the plaintiff initiates the legal case.

For example, let’s say on January 1, 2020, I accidentally chopped off a patient’s arm when I meant to suture his finger. The patient then (still hypothetically) sues me on February 1, 2020. Since my employer’s claims-made malpractice policy was in place on both January 1 and February 1, that policy will cover my legal expenses up to the coverage limits.

However, say the hypothetical patient was a fan of The Fugitive and thought it was kind of cool to be a one-armed man. Five years later, a lawyer friend convinces the patient that two arms really are better than one. On January 1, 2025, the patient sues me for malpractice. If I had changed employers or retired in the meantime, thereby ending my employer-sponsored claims-made insurance policy, that policy would not cover my legal expenses.

Tail coverage, formally called extended reporting period, typically covers physicians after a claims-made insurance term ends (eg: due to a job change or retirement). Most medical practices include tail coverage in their physician employment contracts. In the hypothetical case, if the employer maintained my tail insurance through January 1, 2025, that policy would cover the delayed suit.

Physicians Thrive, a financial advisory, explains that “malpractice tail coverage protects you when you are between jobs or just transitioning from one job to another. It also covers you if you are unexpectedly terminated. Medical malpractice claims can take years to surface. Tail coverage ensures that physicians are protected even after their primary malpractice insurance policy has expired.

Tail coverage basically gives you peace of mind for any unexpected claims. Without tail coverage, physicians would be personally liable for any claims made after the policy’s termination, which could result in substantial financial and legal consequences.

Tail coverage is often considered such important protection for both the physician and the patient. Therefore, some state legislatures require you to have tail coverage to practice medicine. The same goes for many hospitals. If you are looking for a job, many employers would rather hire a new doctor with no prior insurance than pay for tail coverage for an incoming physician.”

The crucial problem with tail coverage is that it ends when the purchaser - in this case, the medical group - stops paying the insurance company.

What is occurrence malpractice insurance?

Occurrence malpractice insurance is simple. If the physician is covered when she cares for a patient, she is still covered when that patient sues for malpractice at any point in the future.

Why do most employers prefer claims-made insurance?

Claims-made insurance offers employers two benefits over occurrence:

Delayed payment schedule; and

Shifting risk onto the physician.

According to The Trust Insurance, “From a pricing viewpoint, occurrence policies are more expensive than comparable claims-made policies because they provide coverage for incidents that occurred during the policy year regardless of when the claim is reported. An occurrence policy provides a separate limit for each year protection is purchased.

Claims-made policies are initially significantly less expensive than occurrence policies. The premium for a claims-made policy is lowest during the first year because the policy only covers incidents that occurred in the first year and are reported as claims in that year. The premium increases during the second year because the policy now covers incidents that occurred during the first and second years as long as the claim is reported during the second year. The claims-made premium continues to increase as the policy matures for 5 to 7 years when the premium usually stabilizes.

The reason it takes a long time for the claims-made rates to mature is that several years can elapse from the time the incident occurred to the time the incident becomes a claim.”

When risk-shifting matters

Under most circumstances, the long-term cost and long-term coverage of claims-made plus tail malpractice insurance converge with occurrence coverage. Both types of insurance are designed actuarially to cover the same financial risk from lawsuits over the same extended time period.

However, claims-made and occurrence coverage diverge massively if an employer can no longer pay its debts and declares bankruptcy. While occurrence policies remain as long as the insurance company survives, claims-made with tail coverage ends when the employer stops paying its bills.

As you can see in the following graphics, large malpractice insurance companies are generally stable financially, while the credit of some of the largest emergency medicine employers is rated B or C by Moody’s (“high credit risk”).

A medical practice’s bankruptcy proceeding rarely salvages employed physicians’ claims-made plus tail coverage. Tail coverage owed to physicians becomes a liability of the insolvent practice. This obligation is treated as a general unsecured debt — the same category as unpaid rent, utilities, or vendor invoices. As lenders are considered secured creditors in bankruptcy, insufficient funds are usually left to cover a significant amount of unsecured debt.

The law firm Weiss Zarett Brofman Sonnenklar & Levy, P.C. concludes, “In our experience through the representation of physicians in bankruptcy cases involving various hospitals, it is not unusual for physicians or residents to learn – unfortunately, after the fact – that hospitals have provided insufficient or no medical malpractice insurance despite being promised in the employment contract. In some cases, the hospital held itself out as ‘self-insured,’ but did not segregate the funds needed to actually cover malpractice claims. In other cases, there was inadequate funding to purchase tail coverage.”

When a medical practice stops paying its insurance carrier for a claims-made with tail policy, the previously employed physician is left with a choice:

Purchase tail coverage individually; or

Go uncovered for patients seen while employed by that medical practice.

Tail coverage is not cheap, especially when purchased as an individual. According to Griffith E. Harris, “the average cost of tail insurance can range from 150% to 300% of a physician’s annual malpractice insurance premium.” Estimates for emergency physician tail policies range from $20,000 to $100,000.

Going uncovered exposes the physician to a significant risk of financial catastrophe from a malpractice suit. According to the JAMA article, “Rates and Characteristics of Paid Malpractice Claims Among US Physicians by Specialty, 1992-2014”, the average emergency medicine malpractice claim payout between 2009 and 2014 was $324,052. This cost is in addition to the legal expense of defending the case.

The 2023 American Medical Association report, “Medical Liability Claim Frequency Among U.S. Physicians,” found that 3.3% of emergency physicians had been sued for malpractice in the prior year. Almost half of emergency physicians (46.8%) had a medical liability claim brought against them in their careers to date.

Conclusion

Employed emergency physicians transfer billing rights for their medical care to their employer. An American Physician Partners employment contract stated, “All fees received or realized related to the provision of the Services shall belong to the Practice. Physician authorizes the Practice or its designated billing company to bill and collect all professional fees for Services rendered by Physician as its agent and attorney-in-fact to the extent permitted by applicable law. Physician assigns all rights to such fees to the Practice in consideration for the payments received by Physician under this Agreement.”

For a medical practice to bill for a physician’s services and then not cover her malpractice risk is a breach of responsibility. Choosing an occurrence malpractice insurance policy for its physicians is the simplest way for a medical practice to properly protect its employed clinicians in case of the practice’s insolvency.

Emergency Medicine Workforce Productions is sponsored by Ivy Clinicians - simplifying the emergency medicine job search through transparency.

As a physician recruiter with 20 years of watching staffing groups come and go, your article just feeds the thoughts that make me leery of large delocalised groups. They all seem to start with good intentions then grow bigger and bigger until those good intentions disappear. The original "love of medicine" gets lost in a monster of an organization. Am I being too idealistic, to hope for democratic single-speciality groups to make a comeback?

Maybe organized medicine can pressure these firms to buy a bond to use for tail insurance to protect physicians against bankruptcy?